Are you planning to retire early? If so, you might be curious about how to budget your income and plan your expenses. Early retirees could face inflation. Social Security is another potential wild card. There are many strategies that can help you plan your money. Learn how to jumpstart your financial future. These are just a few examples.

Saving for your early retirement

Budgeting for early retirement requires you to save money for expenses that may not have been considered. Most people budget for basic necessities like food and transportation, but it is important to include fun expenses such as travel. It is important to include costs associated with purchasing a vehicle. Even though you will be living on less after retirement, your food expenses will not change. You may want to take cooking lessons or try entertaining friends and family.

It is also a smart idea to invest some of your income. A good rule of thumb is to invest at least 15 percent of your income into your retirement. You can withdraw money from your retirement accounts before reaching the age of 59 1/2, but you may be charged an early withdrawal fee.

Managing income streams

Management of income streams to early retirement requires you to identify, capture, and manage all income sources that you will have. Social Security benefits and pension distributions will likely be a mainstay of your retirement income, but you should also consider other sources of income as well. These include dividends, real estate investments and minimum distributions.

The best way to manage income streams in early retire is to determine which investments will produce the highest returns. While the income from a lifetime annuity may be the most predictable, it is also subject to fluctuations due to inflation. It is crucial to take regular, strategic withdrawals that are based on your cash flow needs. Another way to build a steady income stream is by investing in a CD ladder and bond ladder. Annuities that convert a lump sum to an ongoing income stream are a low-risk investment. This way, your money is not affected by falling stock prices or falling interest rates.

Inflation is a financial enemy

Inflation is an important aspect of planning for early retirement. This financial enemy can sap your savings purchasing power and can cause financial instability if you don't plan. Many retirees are living on fixed incomes and are therefore especially vulnerable to the impact of inflation. There are many ways to reduce the impact of inflation on your savings. It is possible to protect your nest egg against the inflation ravages by investing and managing your spending.

In order to offset the inflation effects, early retirees can invest in various types of equities. They should set up their own pension plan if they do not have one from their employer. This option offers the benefit of not having to pay taxes on earnings or investment gains. Early retirees should instead focus on building their portfolio and not relying on fixed annuities or pensions.

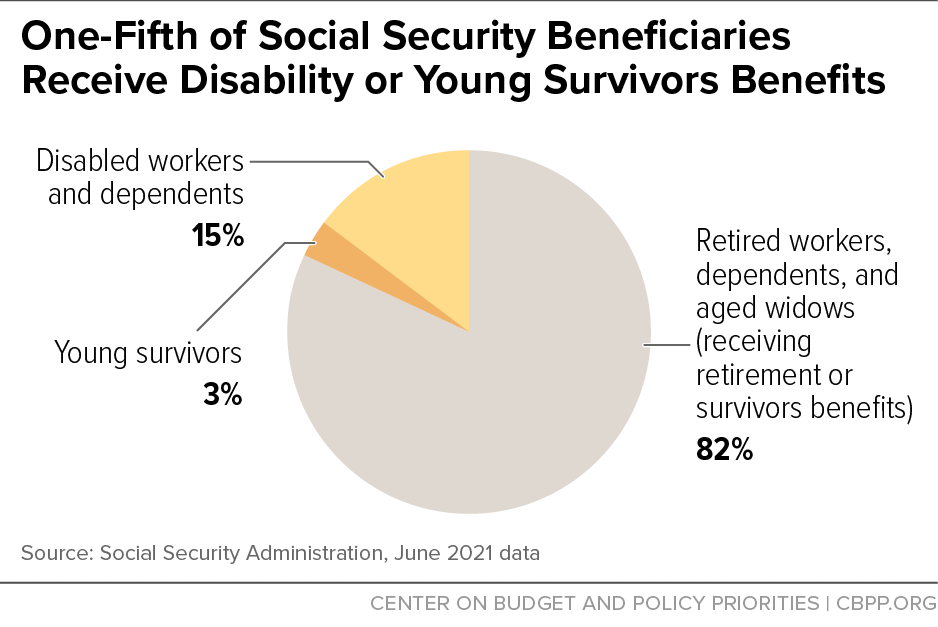

Social Security as a wildcard in early retirement

Social Security Administration, or SSA, uses the "Retirement Earnings test" to determine if a beneficiary has enough time to receive all their benefits before they retire. This test allows SSA withhold benefits from beneficiaries that claim early. To avoid this wild card, you should save more for retirement.

Many early retirees are tempted to get their benefits earlier, particularly for those who were affected by Great Recession. However, a recent study by the Center for Retirement Research at Boston College found that only 5% of eligible people were receiving their checks before the full retirement age. Even if you are concerned about the funding of your retirement, there are ways to address this problem. You can spend less money before retiring and delay retirement until you reach full retirement.

FAQ

How to Start Your Search for a Wealth Management Service

Look for the following criteria when searching for a wealth-management service:

-

Can demonstrate a track record of success

-

Is based locally

-

Consultations are free

-

Offers support throughout the year

-

Clear fee structure

-

Excellent reputation

-

It is simple to contact

-

We offer 24/7 customer service

-

Offers a wide range of products

-

Low fees

-

There are no hidden fees

-

Doesn't require large upfront deposits

-

You should have a clear plan to manage your finances

-

Transparent approach to managing money

-

Allows you to easily ask questions

-

You have a deep understanding of your current situation

-

Understand your goals and objectives

-

Would you be open to working with me regularly?

-

Work within your budget

-

Has a good understanding of the local market

-

Would you be willing to offer advice on how to modify your portfolio

-

Is willing to help you set realistic expectations

What is retirement planning exactly?

Retirement planning is an important part of financial planning. It allows you to plan for your future and ensures that you can live comfortably in retirement.

Planning for retirement involves considering all options, including saving money, investing in stocks, bonds, life insurance, and tax-advantaged accounts.

What Are Some Examples of Different Investment Types That Can be Used To Build Wealth

There are many different types of investments you can make to build wealth. Here are some examples.

-

Stocks & Bonds

-

Mutual Funds

-

Real Estate

-

Gold

-

Other Assets

Each has its own advantages and disadvantages. Stocks and bonds, for example, are simple to understand and manage. However, they can fluctuate in their value over time and require active administration. Real estate, on the other hand tends to retain its value better that other assets like gold or mutual funds.

Finding something that works for your needs is the most important thing. It is important to determine your risk tolerance, your income requirements, as well as your investment objectives.

Once you have chosen the asset you wish to invest, you are able to move on and speak to a financial advisor or wealth manager to find the right one.

Statistics

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- According to Indeed, the average salary for a wealth manager in the United States in 2022 was $79,395.6 (investopedia.com)

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

External Links

How To

How to save on your salary

Working hard to save your salary is one way to save. These steps are essential if you wish to save money on salary

-

It's better to get started sooner than later.

-

Reduce unnecessary expenses.

-

You should use online shopping sites like Amazon, Flipkart, etc.

-

You should do your homework at night.

-

Take care of yourself.

-

It is important to try to increase your income.

-

A frugal lifestyle is best.

-

You should learn new things.

-

Sharing your knowledge is a good idea.

-

Regular reading of books is important.

-

Make friends with rich people.

-

Every month you should save money.

-

Save money for rainy day expenses

-

It's important to plan for your future.

-

It is important not to waste your time.

-

You should think positive thoughts.

-

Negative thoughts are best avoided.

-

Prioritize God and Religion.

-

It is important to have good relationships with your fellow humans.

-

Enjoy your hobbies.

-

You should try to become self-reliant.

-

Spend less than you earn.

-

You should keep yourself busy.

-

Patient is the best thing.

-

Remember that everything will eventually stop. It is better not to panic.

-

You shouldn't borrow money at banks.

-

Problems should be solved before they arise.

-

It is a good idea to pursue more education.

-

It's important to be savvy about managing your finances.

-

It is important to be open with others.